Traditionally, income tax has always been based on percentage of net income. The problem here is that it cannot be infinitely progressive because as tax rates approach 100% in a linear fashion, net income after taxes would peak and then eventually drop to zero. Furthermore, one first has to determine the tax rate before arriving at net income after taxes. Why not save a step and let net income before taxes itself directly determine net income after taxes?

Here we introduce the remaining income method, which will not only make it easier to determine net income after taxes, but will also provide an infinitely progressive scale of taxation. Simply put, net income after taxes will be provided be the following equation:

a = m + [√(bm) * ln (b/m)], where

- a = net income after taxes

- b = net income before taxes

- m = minimum wage

Because this equation is based on minimum wage, it is resistant to the effects of inflation and increase in cost of living, as explained here.

It can be seen in this equation that a minimum wage earner would have a net income of exactly minimum wage and would hence not pay any taxes. Furthermore, using calculus, it has been determined that the maximum slope of this equation is 1 and it occurs where a=b=m, which means everybody earning above minimum wage will pay taxes.

This equation assumes that everyone earns at least minimum wage. Otherwise, the equation would not work. In any case, nobody should earn below minimum wage.

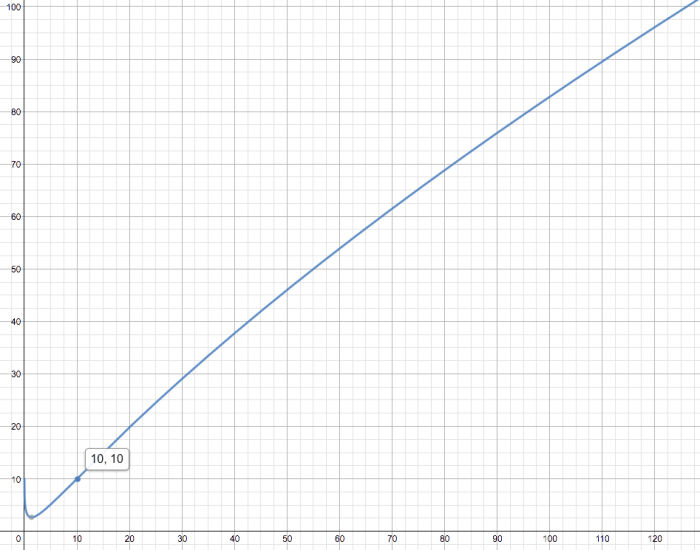

A graph for this equation at a minimum wage of $10/day would look like this:

It can be seen it this graph that person who earns the minimum wage of $10 (x-axis) would keep all $10 (y-axis). On the other hand, someone earning $100 would keep over $80. Let us zoom out to include net incomes up to $1,000:

Now we see that the graph has become flatter. A $200 earner can keep just under $150; someone with a $500 wage keeps just under $300. At $1,000, you get to keep less than half of your wages, but that’s still nearly fifty times the minimum wage earner.

Let us now plot these values in Excel to better understand them:

As can be seen here, if you earn $100,000 or 10,000 times the minimum wage, you are taxed at around 91% and keep around $9,000, which is 900 times the minimum wage. Likewise, if you earn an insane 10 MILLION times the minimum wage PER DAY ($100,000,000), you are also taxed at an insane rate of 99.49%, yet you still get to keep $500,000, which is still 50,000 times the minimum wage. To put that into perspective, a minimum wage earner would have to work every day for 137 years to earn $500,000.

At higher income strata, tax deductions from income is no longer important. What matters is you have much more than enough to live a comfortable life many times over.

With this kind of taxation, governments in countries where income inequality is high may be able to collect more taxes, which can be used for projects that can alleviate poverty such as infrastructure, health and education. Consumption taxes may be lowered as well or even removed, further giving lower income families more purchasing power. Likewise, a highly equitable society would pay less taxes, and its government would not need to be too big.

You must be logged in to post a comment.